Cigna Global Health Insurance Review: Is It Worth It? (2026)

Is Cigna Global worth the premium? Read our honest 2026 review. We break down the Silver, Gold, and Platinum tiers, actual pricing, and visa compliance.

If you are a long-term expat, a remote worker on a residency visa, or a digital nomad applying for a Digital Nomad Visa, you need more than travel insurance. You need International Private Medical Insurance (IPMI) that functions like your home country health plan, just with global coverage.

Cigna Global is one of the most recognized and comprehensive IPMI providers available. I have used Cigna personally and spent time reviewing every tier, add-on, and the claims process in detail. This review covers everything you need to know: the plan tiers, real pricing ranges, visa compliance, and what the experience is actually like when you need to make a claim.

Here is my complete, honest verdict.

Cigna Global Options: Key Details at a Glance

- 💰 Annual Limits: $1M (Silver), $2M (Gold), Unlimited (Platinum)

- ✅ Deductibles: Customizable from $0 to $10,000

- 🌐 Hospital Network: 1.5+ million doctors and facilities globally

- 🧾 Pre-existing conditions: Covered subject to individual underwriting

- 🇪🇺 Visa eligibility: Silver plan with $0 deductible accepted for Spain, Portugal, and Greece Digital Nomad Visas

- 📊 Trustpilot: 4.1 / 5 stars (3,500+ reviews)

- ⚠️ Not available to residents of: Hong Kong, Singapore, Thailand, Indonesia, or Kenya

What type of insurance is Cigna and is it good?

Cigna Global is considered by many to be one of the most established IPMI providers on the market, particularly among American expats, long-term travelers, and digital nomad visa applicants.

It is not a travel insurance plan. Cigna Global is designed to work as your primary health insurance while you live abroad. It covers routine care, specialist visits, surgeries, cancer treatments, and mental health, depending on the tier and add-ons you select.

What makes Cigna stand out is the customization. During the quote process, you can adjust your deductible (from $0 to $10,000), choose your cost-share percentage, set a payment schedule, and pick modular add-ons. This level of flexibility is almost unheard of at this tier of coverage.

Their Trustpilot rating of 4.1 out of 5 stars across more than 3,500 reviews reflects consistently strong satisfaction, especially for claims processing and 24/7 multilingual customer support.

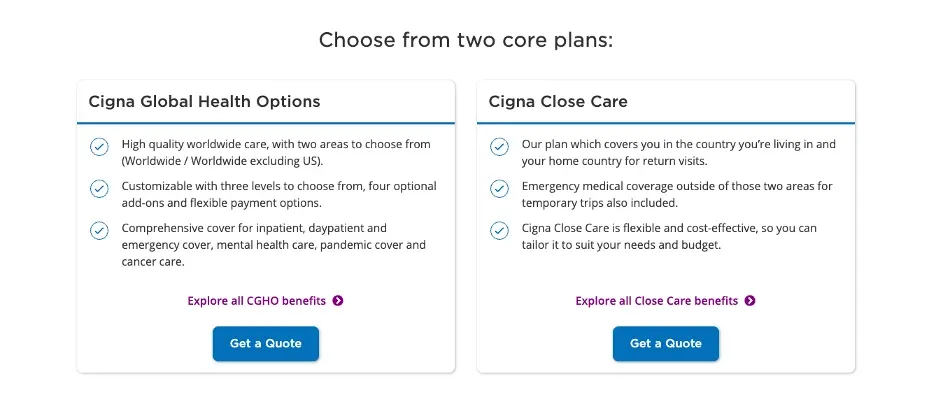

Cigna Global Health Options vs. Cigna Close Care

Cigna Global offers two distinct product families that are completely separate in structure and purpose. Understanding the difference is critical before you choose a plan.

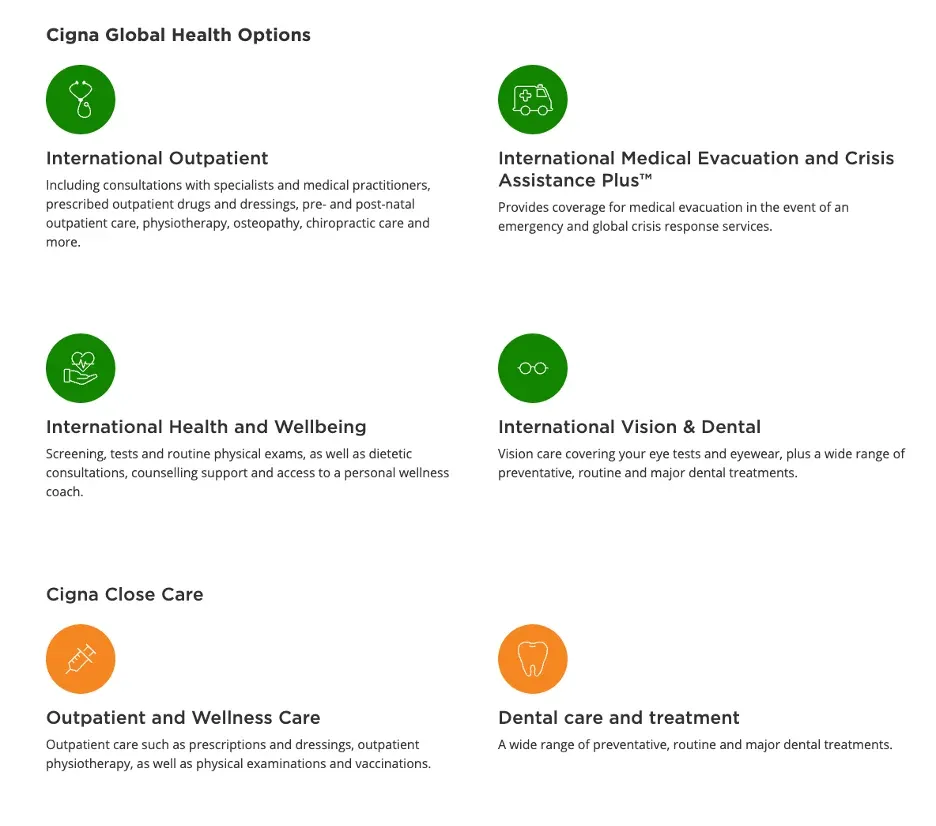

Cigna Global Health Options

Cigna Global Health Options is their worldwide flagship IPMI. It comes in three tiers: Silver, Gold, and Platinum. This is the product line designed for expats, long-term nomads, families abroad, and digital nomad visa applicants who need full primary health insurance coverage.

All three tiers include inpatient care, cancer care, emergency room treatment, evacuation, and medical imaging. The differences between tiers are in annual limits, maternity benefits, outpatient sub-limits, and imaging caps.

Cigna Close Care

Cigna Close Care is a separate, standalone regional plan with a single tier and a strict $500,000 annual benefit cap. It is designed specifically for expats who live in one target country and occasionally return home. Close Care covers you in your country of citizenship and your country of residence, with emergency-only coverage during short trips outside those two zones.

It does not come in Silver, Gold, or Platinum tiers. It is one plan at one coverage level. Its main advantage is price: starting around $117 per month for younger expats, it is the most affordable Cigna product. But given its geographic restrictions and the $500,000 cap, it is not suitable for nomads or multi-country travelers.

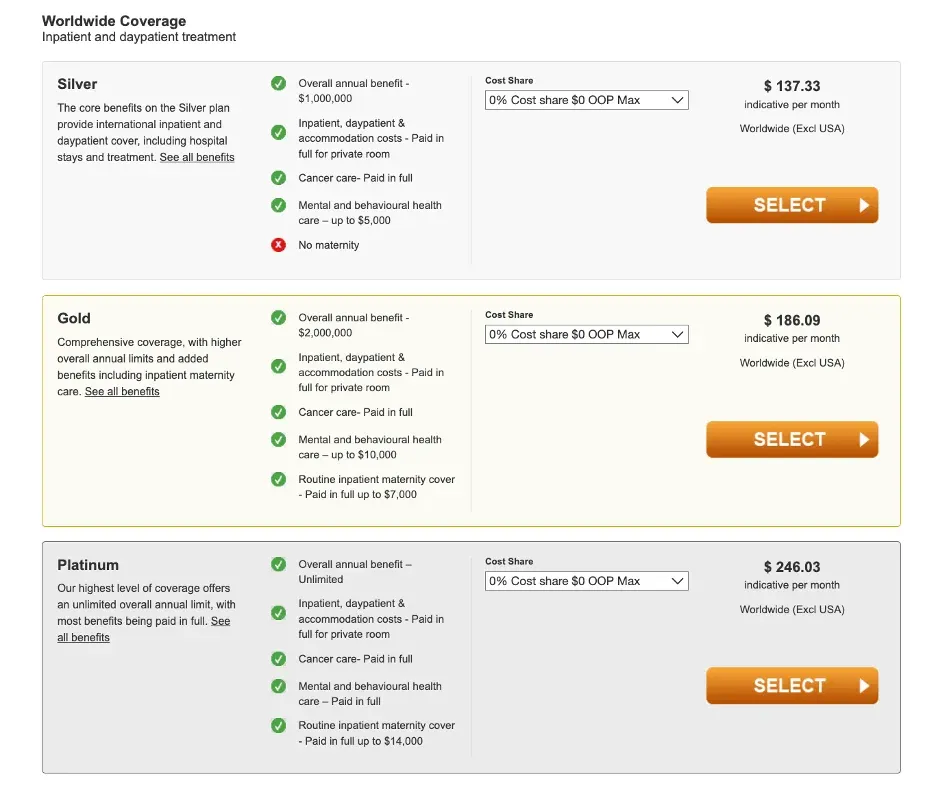

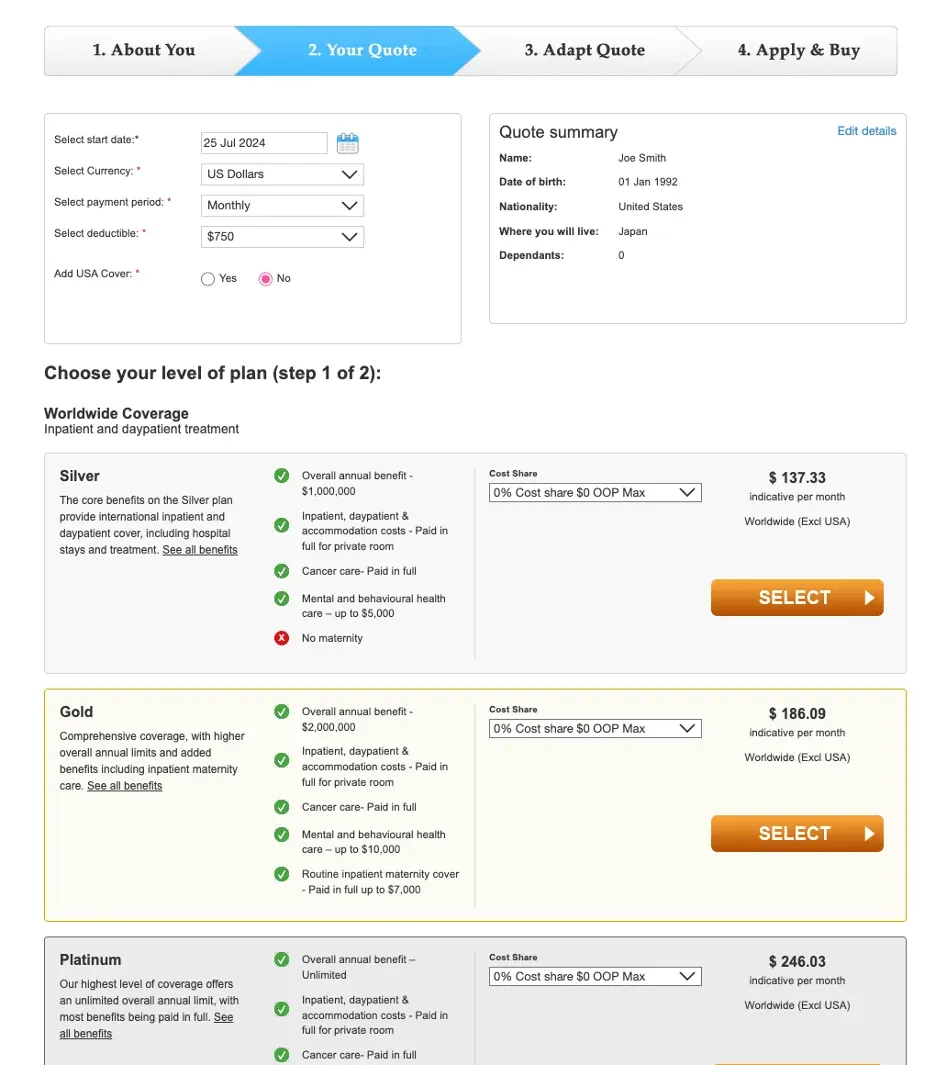

Breaking Down Cigna's Tiers: Silver vs. Gold vs. Platinum

Here is a clear breakdown of what each Cigna Global Health Options tier covers:

| Feature | Silver | Gold | Platinum |

|---|---|---|---|

| Annual Overall Limit | $1,000,000 | $2,000,000 | Unlimited |

| Inpatient / Day-patient | Full coverage | Full coverage | Paid in full |

| Cancer Care | Up to $1M limit | Up to $2M limit | Paid in full |

| Medical Imaging Cap | $10,000 | $30,000 | Unlimited |

| Routine Maternity | Not included | Up to $7,000 | Up to $14,000 |

| Rehabilitation | Included | Included | Paid in full |

| Best For | Digital nomad visa applicants, cost-conscious expats | Families, expats planning maternity | Long-term expats wanting maximum coverage |

Factual Pricing and How to Keep Costs Low

Cigna Global premiums vary significantly by age, location, deductible, and coverage area. To give you a concrete reference point, here are realistic monthly pricing ranges for a 35-year-old expat on the Silver, Gold, and Platinum plans with a $0 deductible and worldwide coverage excluding the US:

- Silver: ~$186 / month

- Gold: ~$312 / month

- Platinum: ~$478 / month

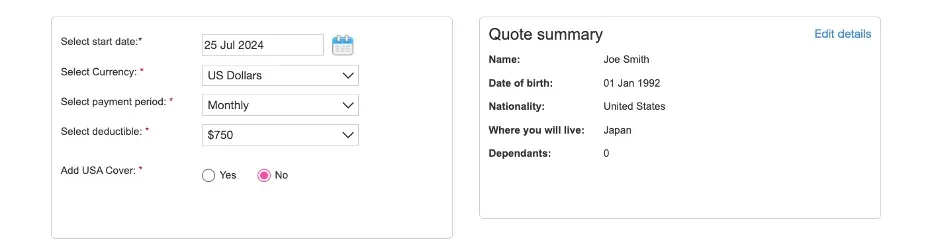

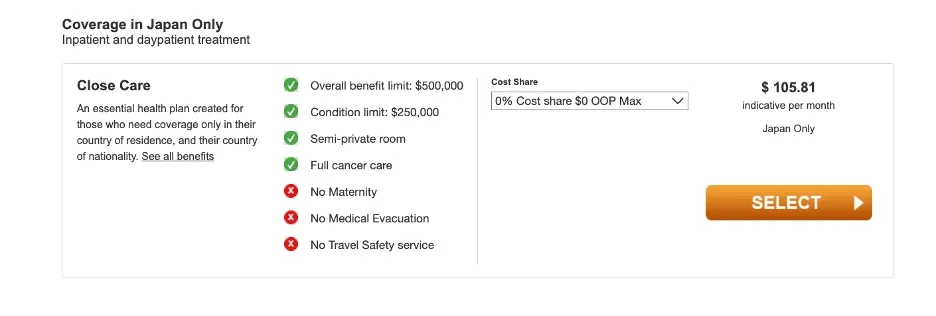

These prices will be substantially higher if you include US coverage in your zone. Here is a real quote sample for a 32-year-old American for a long-term stay in Japan:

Here are the worldwide coverage options and monthly prices:

And here are the Japan-only coverage options and monthly prices:

Add-ons will increase your premium further:

Four Ways to Lower Your Cigna Premium

- Exclude the United States from your coverage area. This is the single most powerful lever. Choosing a "Worldwide excluding the US" zone typically reduces premiums by 50 to 70 percent. If you are not planning to visit the US, this is a no-brainer.

- Choose a voluntary deductible. You can select a deductible from $375 up to $10,000. A $1,000 or $2,500 deductible noticeably reduces your monthly payment while still protecting you against large medical bills.

- Adjust your cost-share percentage. Accepting up to 30 percent cost-share (with a $5,000 out-of-pocket cap) lowers your premium while capping your worst-case exposure.

- Pay annually. Choosing an annual payment schedule instead of monthly typically saves around 5 percent over the course of the year.

My Experience Using Cigna

I have used Cigna as my primary health insurance while living abroad, and the feature that stands out most is the customization during the quote process. Few IPMI providers let you adjust this many variables: start date, currency, payment frequency, deductible, cost-share percentage, and out-of-pocket maximum, all before you commit.

During a stay in Bali, I needed treatment for a severe case of food poisoning. The claims process was straightforward: I paid out of pocket at a local clinic, submitted the invoice and medical report through the online portal, and received reimbursement within the processing window. For a condition that would have cost a small fortune without coverage, Cigna did exactly what it was supposed to do.

What I appreciate most is knowing that as a long-term expat, I have a plan that handles both emergencies and ongoing care, not just trip interruptions. That peace of mind is the core value proposition of Cigna vs. cheaper travel insurance alternatives.

Digital Nomad Visa Compliance: Spain, Portugal, Greece

If you are applying for a Digital Nomad Visa in Spain, Portugal, or Greece, your immigration attorney will tell you the same thing: your health insurance must function as primary medical coverage with no copays and a $0 deductible. It cannot be a travel policy or supplementary plan.

Cigna Global Health Options Silver with a $0 deductible is one of the most widely accepted plans for this purpose. It satisfies the requirements of the Spanish Ley de Startups visa, the Portuguese Digital Nomad Visa (D8), and the Greek Digital Nomad Visa because:

- It functions as primary health insurance, not travel insurance

- A $0 deductible option is available, meaning no out-of-pocket costs for covered care

- The $1M annual limit comfortably exceeds consulate minimums

- Coverage is worldwide with no restrictions on which EU country you are in

Some Things to Keep in Mind About Cigna

No insurance company is perfect. Here are the most important things to understand before you commit to a Cigna Global plan.

The Close Care Plan Is Geographically Restricted

Cigna Close Care is not a worldwide plan. It covers you only in your country of citizenship and your country of residence, with emergency-only coverage during short trips outside those two zones. There is no A and E coverage, no transplant coverage, and a hard $500,000 annual cap. If you are a nomad crossing multiple countries, this plan is not suitable for you.

Waiting Periods May Apply

Many Cigna Global benefits come with waiting periods. The Cigna Global Health Platinum plan has waiting periods for the following:

- Up to 12 months for pre-natal and post-natal care

- Up to 24 months for infertility investigations and treatments

- Up to 12 months for genetic cancer testing

- 3 to 18 months (depending on the service) for dental treatments

- Up to 12 months for routine maternity care, maternity complications, homebirths, and newborn care

Pre-existing Conditions Are Subject to Individual Underwriting

Some Cigna Global plans can cover pre-existing conditions, particularly for applicants over 60 or those who go through full medical underwriting. However, this is not guaranteed and depends entirely on the outcome of your medical history review.

If you have a condition you need covered, discuss it directly with a Cigna representative before signing up. You can find relevant information on their expat insurance page and their international insurance for people working abroad page.

Addressing the Red Tape: What New Members Should Know

Cigna Global is an institutional IPMI provider, and that means it operates with institutional processes. Before undergoing a planned procedure, an MRI scan, or an elective hospitalization, you are required to contact Cigna for prior authorization.

If you skip this step and go ahead with the procedure anyway, Cigna may apply a co-insurance penalty or reduce your reimbursement, even for covered treatments. This is standard practice across serious IPMI providers, but it catches members off guard if they are coming from simpler travel insurance products.

The good news is that Cigna operates a 24/7 multilingual customer care line. Calling before any significant medical event is straightforward, and their team will confirm coverage, locate a nearby network facility, and in many cases set up direct billing so you do not have to pay out of pocket and wait for reimbursement.

For emergency and urgent care, you do not need prior authorization. Show up, get treated, and file the claim afterward.

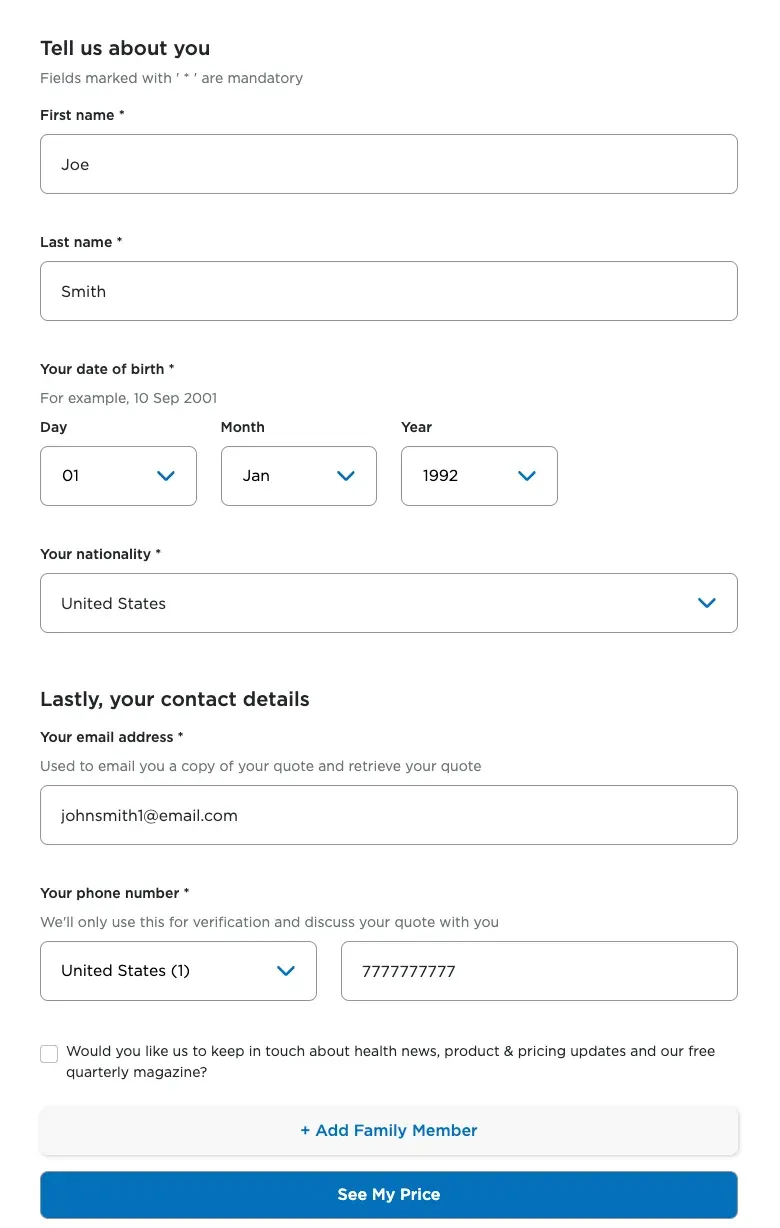

How to get a Cigna health insurance quote

You could get a quote from Cigna in your sleep, well, not really, but you get the point. Here are some quick steps to follow:

Step 1: Go to the Cigna Global quote page

Step 2: Enter the country you’ll be living in for the duration of the policy and click Get a free quote

Step 3: Fill out this form and then click the See my price button.

Step 4: You’ll then be able to see the prices and benefits of all the plans. Set the terms you want and then click Select next to your desired plan.

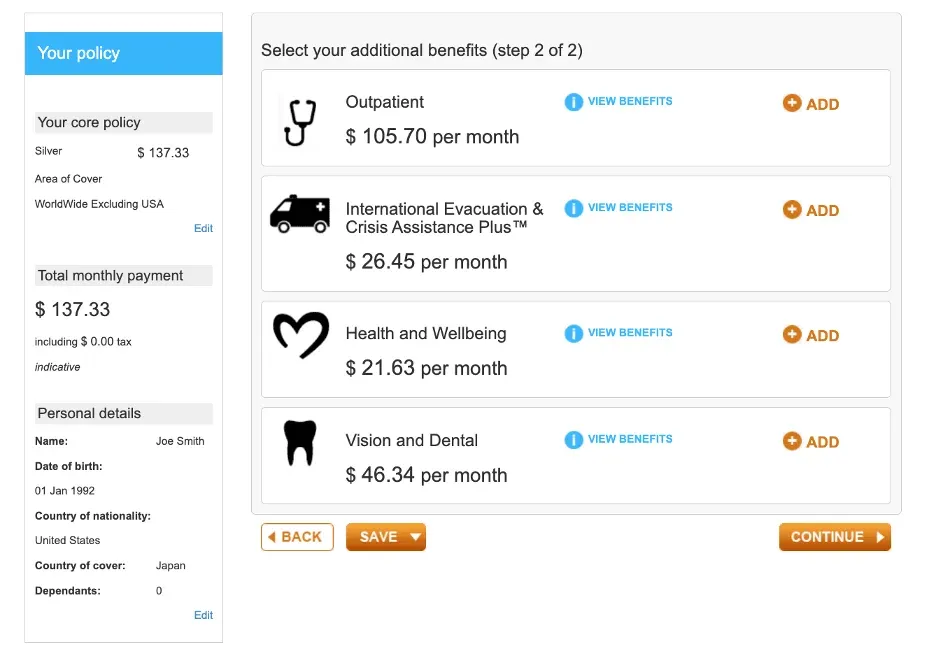

Step 5: Add your add-ons if desired by clicking “ADD.” Then click “Continue” on the bottom right.

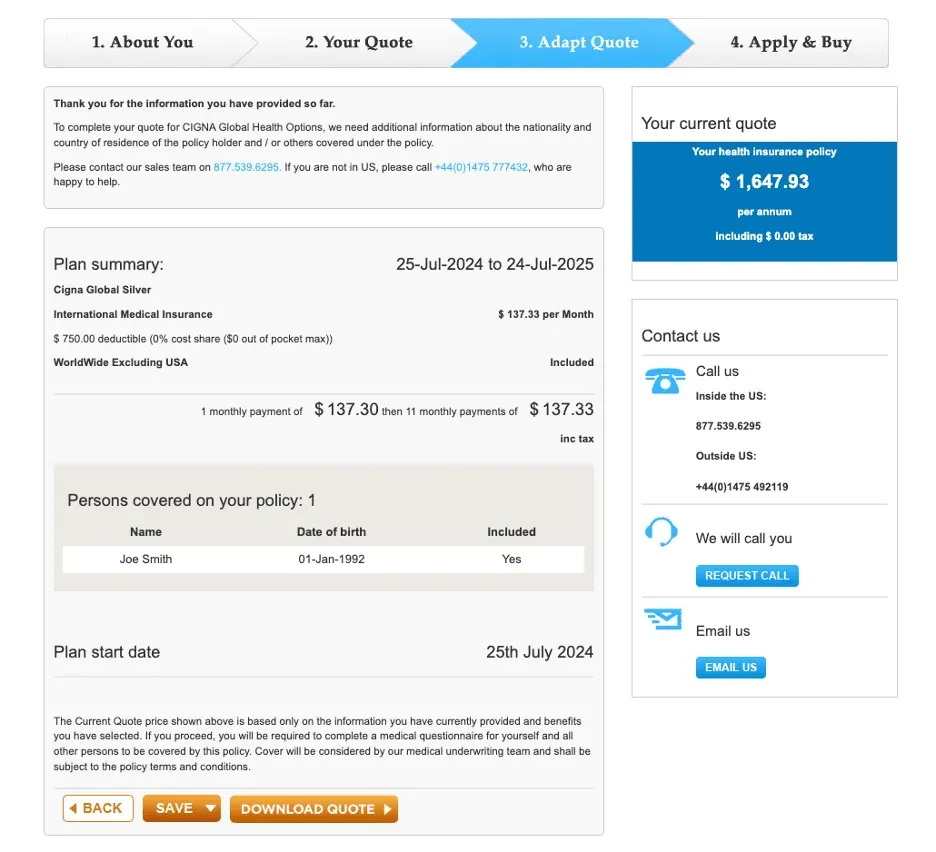

Step 6: View your final price. In some cases, you’ll be able to pay for your policy right then and there. And in other cases, you’ll be instructed to reach out to Cigna to complete the process.

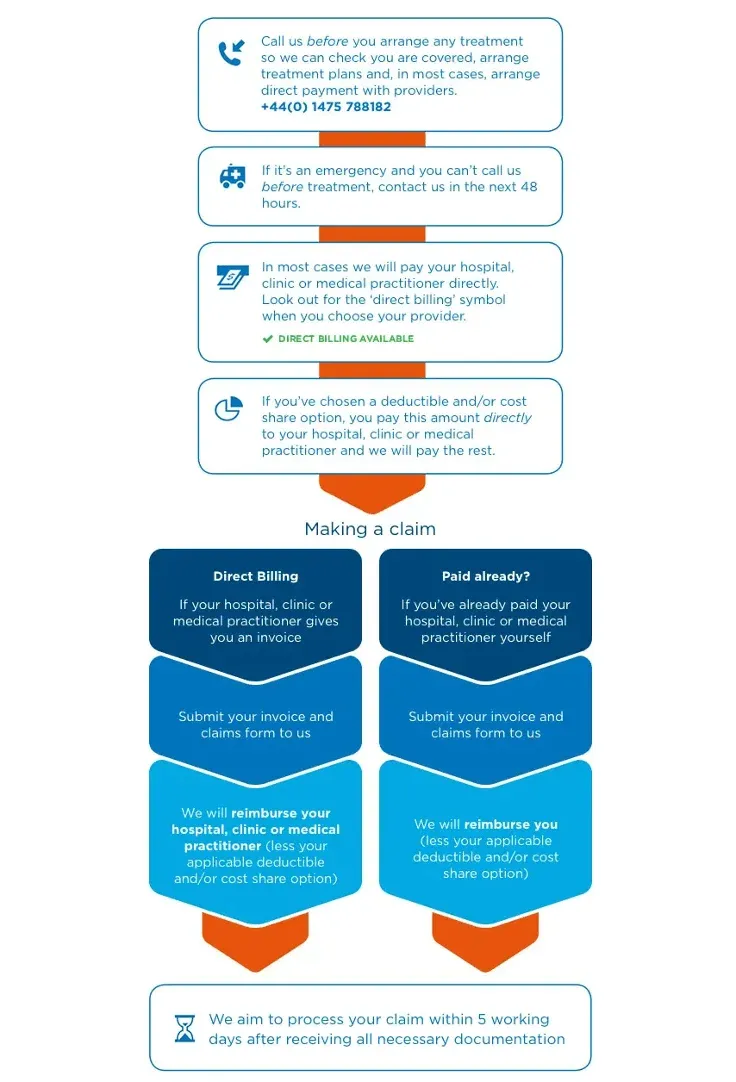

How is the Claim Process for Cigna?

There are a few things I would recommend you keep in mind when submitting a claim to Cigna. Here are my best tips:

- Call customer care whenever you need treatment. Cigna reps will help you find the right healthcare professionals and facilities. They will also set up direct billing if possible.

- Send in a claim to Cigna if needed. If Cigna billed the provider directly, you don’t have to send an invoice or claim form to Cigna. If you paid for your treatment and need reimbursement, you’ll send 1) the invoice from the provider and 2) a claim form to Cigna. Email them to cghoclaims@cigna.com, fax them to +44 (0) 1475 492113, or mail them to Cigna Global Health Options, Customer Service, 1 Knowe Road, Greenock, Scotland, PA15 4RJ. You can also send in claims using your online portal account, which you’ll gain access to after buying a policy.

- For medical and vision claims, you can use this claim form while for dental claims, use instead this claim form.

- Wait for a payment, denial, or documentation request. Claims are typically processed within five working days.

Here’s a handy graphic to make the claims process easier to visualize:

Pros and Cons of Cigna Global

Based on my experience using Cigna as a long-term expat and reviewing the full product line:

Alternative Expat Insurance Options to Consider

Cigna is an excellent choice, but it is not the only strong option in the IPMI space. Here are the main alternatives:

Genki Native

Genki Native is one of the most popular insurance options for digital nomads. They are known for comprehensive medical benefits, fast signup, and quick reimbursement. Cigna edges out Genki when it comes to customization and the breadth of its provider network, but Genki tends to be more straightforward to purchase and manage online.

SafetyWing Nomad Insurance Complete

SafetyWing Nomad Insurance Complete is a strong mid-tier IPMI with a cleaner digital experience and lower entry price than Cigna. It covers routine care, mental health, and emergencies, but its limits and customization do not match Cigna's upper tiers. If budget is a primary concern and you want something between travel insurance and full IPMI, it is a solid choice.

GeoBlue

GeoBlue offers an international insurance network spanning 190+ countries with telehealth capabilities and competitive pricing. GeoBlue has more plan variety with moderate customization, whereas Cigna has fewer plans but deeper configurability. For US citizens in particular, GeoBlue is a strong Cigna alternative.

For a full side-by-side comparison of all major IPMI options, see our guide to the best international health insurance for digital nomads. You can also compare SafetyWing and SafetyWing vs World Nomads for travel-focused alternatives.

Cigna insurance FAQs

Does Cigna cover Wegovy?

Yes, many Cigna plans now include Wegovy, especially after they introduced a pharmacy add-on that caps your out-of-pocket expense at $200/month for Wegovy and Zepbound. Still, coverage depends on your specific plan and doctor approval.

Does Cigna cover Zepbound?

Often yes, but it usually requires prior authorization. Coverage depends on meeting clinical criteria and may exclude if you're already on a similar weight-loss drug.

Does Cigna cover therapy (mental health)?

Yes, many Cigna plans include mental health services like therapy, counseling, and psychiatric care. However, check your specific plan for session limits and in-network provider options.

Does Cigna cover Invisalign?

Yes, some Cigna dental plans include orthodontic benefits like Invisalign or braces. Coverage is usually partial (e.g., 50%), and subject to a lifetime maximum.

Is Cigna HMO or PPO?

They offer both. Cigna provides flexible plan models (HMO, PPO, EPO, etc.), so you can choose based on how much freedom and network flexibility you want.

Does Cigna cover Mounjaro?

Mounjaro (a newer GLP-1 drug) likely follows the same rules as Wegovy/Zepbound. Coverage depends on your plan’s formulary and if your doctor meets the guidelines and prior authorization is typically required.

Will Cigna cover Wegovy for weight loss?

Yes, but only if it’s prescribed according to FDA-approved uses (BMI > 30 or BMI > 27 with related conditions) and meets plan requirements.

Does Cigna cover dental implants?

Maybe, but it depends on your dental plan. Basic plans often don’t, but full dental or dental-plus plans may cover implants partly. Check your specific coverage details.

Is Cigna a private insurance?

Yes, it’s private health insurance. They offer individual, family, and international health plans, not government-run like Medicare or Medicaid.

Does Cigna cover gym membership?

Sometimes. Some plans include wellness perks or HSA-eligible fitness reimbursements. It varies, so check your specific plan.

Is Cigna Medicare?

Cigna offers Medicare Advantage plans through its Cigna Healthcare subsidiaries. They also coordinate with the government Medicare parts but are not the Medicare program itself.

Is Cigna Medicaid?

No, Cigna doesn’t administer Medicaid. They only offer private insurance and Medicare Advantage options.

Which Cigna plan covers IVF?

Some global health and comprehensive employer plans offer fertility benefits, including IVF. It depends heavily on the specific plan and location, so you’d need to check your plan documents or ask your rep.

Will Cigna cover my abortion?

Yes, most private Cigna plans include both elective and therapeutic abortion services, though coverage may vary by state and plan.

Ready to get to your next destination with extra peace of mind?

Find places, workspaces, events and a community that gets you.

Get Freaking Nomads Pro

Andrea is a copywriter with 10+ years experience writing SEO-friendly B2B and B2C content. She writes and edit copy in the travel, healthcare, insurance, finance, business, and beauty niches.

Freaking Nomads is supported by you. Clicking through our links may earn us a small affiliate commission, and that's what allows us to keep producing free, helpful content. Learn more

Read Next

Best Laptop-Friendly Cafés in Gran Canaria to Work From

10 Tips to Save Money on Rental Cars When Traveling